I’ve written about this before but now is a timely time to talk about it again, with tax season underway.

I prepare a lot of individual tax returns, and one of the most-common compliance issues I see is: people contributing too much into their Roth IRA. One-hundred percent of the time, the person had no idea there was a problem.

IRAs

There are two types of individual retirement accounts you can open – a traditional IRA and a Roth IRA.

- Traditional IRA: deposits (usually called “contributions”) into the plan are tax deductible (usually); withdrawals are (usually) taxable. Not the use of a lot of parenthetical references here. More shortly.

- Roth IRA: deposits are not tax deductible. The flip side is, withdrawals are not taxable at all (as long as the withdrawals are considered qualified).

Now, what is this about “over-deposits” into a Roth IRA?

Contribution Limits

Tax law specifies a maximum amount that you can contribute to an IRA in a year. The limits are:

- 2023: $6,500 ($7,500 if age 50+)

- 2024: $7,000 ($8,000 if age 50+)

This is an overall IRA limit, so if you want to contribute to both a traditional IRA and a Roth IRA, the limit is $6,500 ($7,500) in 2023 overall.

So, again, what is this about “over-deposits” into a Roth IRA? This is a lot of setup. Well, the setup is important to answering the question.

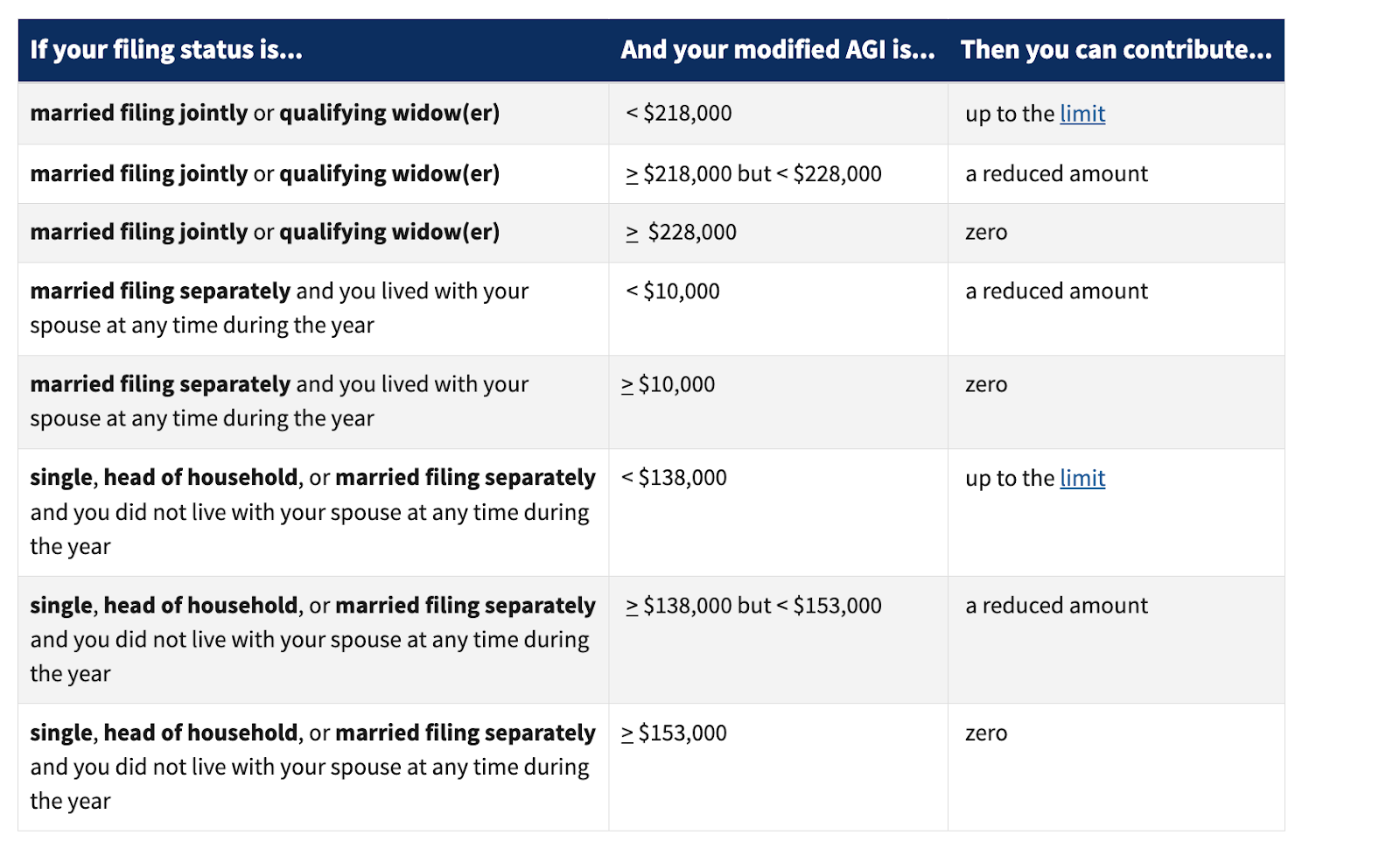

AGI Restrictions

Adjusted gross income (AGI) restrictions apply to contributions to an IRA.

In a traditional IRA, those AGI restrictions apply only to the deductibility of contributions into the IRA. You can make the full contribution, but if your AGI is too high (and you are covered by a retirement plan at a job) you might not be able to take a deduction for the contribution. This is a different blog post for a different day.

Now, we finally answer the question about what’s going on with over-contributions to Roth IRAs.

The AGI restrictions relating to Roth accounts actually restrict your ability to put money into the account. From the IRS:

Real World Scenarios

It is very easy for people to run afoul of the Roth IRA AGI restrictions.

Things I have seen:

- People start a Roth IRA on their own, knowing nothing about the AGI restrictions and they don’t tell me about it until sometime later … and their income has always been above the AGI limits.

- People whose investment advisor opens a Roth IRA for them, and the advisor doesn’t tell them about the AGI limits.

- People who have a Roth IRA, and whose income has always been below the AGI thresholds … until this year when they received a big pay raise and they’re now past the thresholds.

- People who have a Roth IRA, and they file as married filing separately because of income-based repayment on student loans. I caught this for a new client one time, and we had to fix some 5 or 6 years (I can’t remember exactly how many anymore, it’s been a long time) of over-deposits. Note in the IRS chart above, how ridiculously low the AGI thresholds are for married filing separately.

Fixes

We’ll cover fixes in a future post. But the 30,000-foot view is:

- Leave the over-contribution in and pay a 6% penalty … but this money is “tainted,” meaning the 6% penalty will apply on that over-contribution every year.

- Leave the over-contribution in this year and pay the 6% penalty, and if income drops next year, use it as a contribution in that future year (and no more penalty).

- Withdraw the excess contribution by the due date (including extensions) of the return.

Footnote on Roth 401(k)

People (including tax pros) often ask if these AGI limits apply to Roth 401(k) contributions. The answer is no, they don’t. People of any income level can contribute to a Roth 401(k) through an employer.